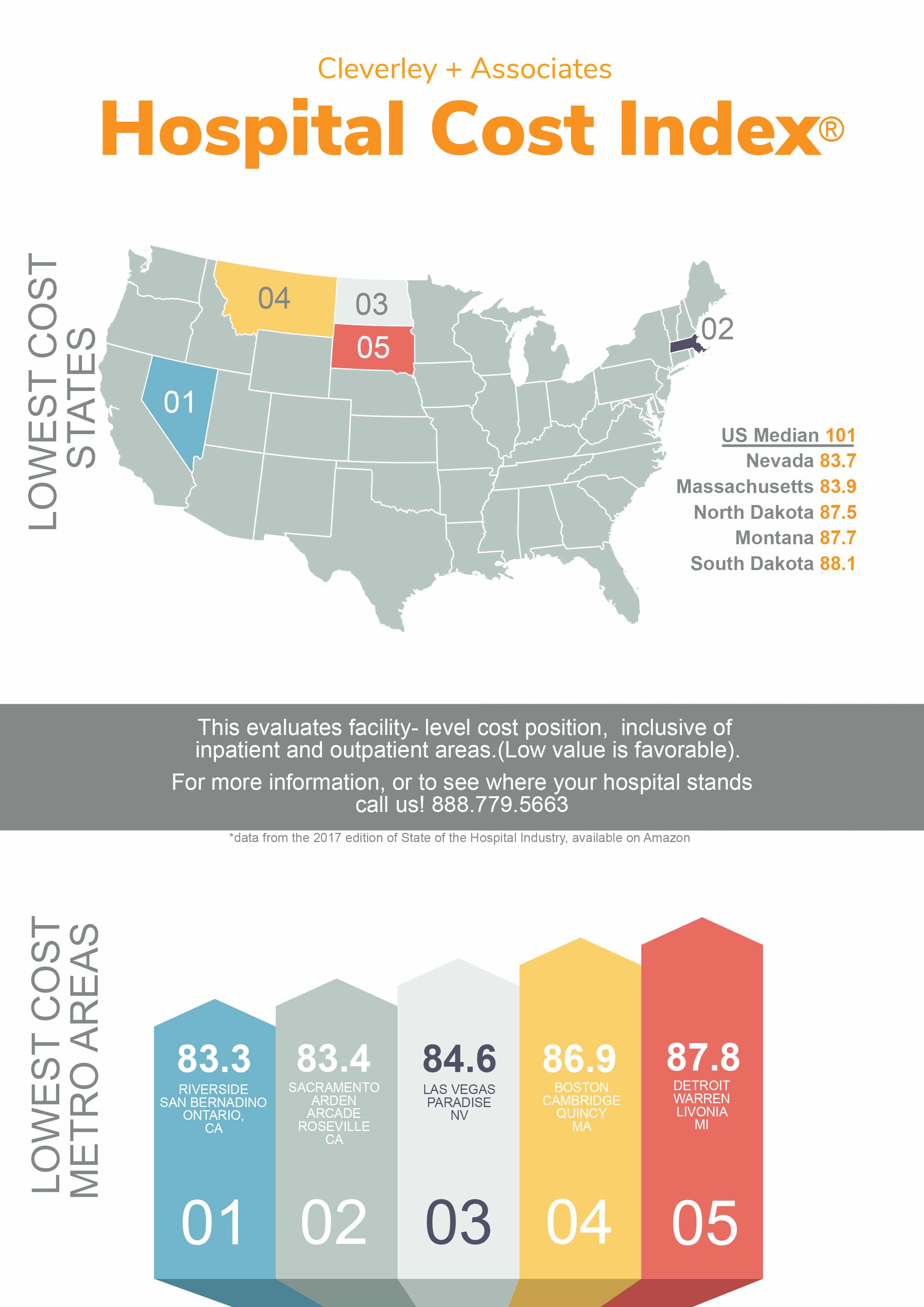

FY 2019 IPPS Final Rule: A Closer Look at Wage Index Changes

To what extent is Wage Index based on payment CBSA changing from FY 2018 to FY 2019?

*Data Source: CMS, FY 2018 & 2019 IPPS Final Rule Impact Files, FY 2019 URSPA variable

*Data Source: CMS, FY 2018 & 2019 IPPS Final Rule Impact Files, FY 2019 URSPA variable

Based on the data above, the clear majority of hospitals are experiencing an increase or decrease less than 5% or no change at all (92%).

Why should hospitals be aware?

Even small changes with wage index (WI) combined with MSDRG relative weight (RW) changes could mean significant payment differences based on a hospital’s case mix. The WI is calculated and assigned to hospitals on the basis of the labor market area in which the hospital is located. WI is updated annually and applied to the labor-related share of the national IPPS base payment rate. A provision of the Act requires updates or adjustments to the WI be made in a manner that ensures aggregate payments to hospitals are not affected by the change in the WI. However, to an individual hospital, overall change in payment will also depend on changing services and volumes in addition to policy change factors such as Operating Base Payment and MSDRG RWs.

Case Hospital Example: Urban Ohio Hospital with > 10% Decrease in WI

Reviewing the top 3 MSDRGs for an example hospital illustrates a change in payment from 2018 to 2019. In this example, the volumes by MSDRG remain static, with the assumption volumes will remain the same or similar in subsequent years. The other key ingredients to payment include Operating Base Rate and MSDRG RWs in addition to WI.

- FY 2019 Wage Index = 0.8237

- FY 2018 Wage Index = 0.9366

Operating base rate increases from FY 2018 to FY 2019. MSDRG RWs are various in terms of increasing or decreasing from FY 2018 to FY 2019. However, the overall decrease in the WI for this hospital example is showing to drive the decrease in overall payment, especially prominent with MSDRG 871.

*Data Source: CMS, FY 2018 & 2019 Table 5, FY 2018 & 2019 IPPS Final Rule Impact Files, 2017 MedPAR.

1Payment Differences due to WI Changes: FY 2019 Operating base rate and FY 2019 MSDRG Relative Weights to isolate Wage Index impact with static volumes

2Payment Differences due to RW Changes: FY 2019 Operating base rate and FY 2019 Wage Index to isolate Relative Weight impact with static volumes

3Payment Differences due to Operating Base Payment Changes: FY 2019 MSDRG Relative Weights and FY 2019 Wage Index to isolate Operating Base Payment impact with static volumes

4Total Payment Differences: FY 2018 and 2019 Operating base rate, FY 2018 and 2019 MSDRG Relative Weights, and FY 2018 and 2019 Wage Index to illustrate overall payment change with static volumes

What is the Impact to my Hospital?

Assessing the impact to Prospective Payment Rule polices is essential is understanding future Medicare payments. Identifying driving factors could assist the hospital in offering feedback to CMS, budgetary purposes at the facility and departmental levels, or potentially pursuing reclassification designation.

Is Wage Index reclassification beneficial for your Organization?

While the process to reclassify is complex, if a hospital meets the criteria to potentially reclassify to be advantageous, the process may be worth the efforts.

FY 2020 Geographic Reclassification Deadlines:https://www.cms.gov/Medicare/Medicare-Fee-for-Service-Payment/AcuteInpatientPPS/wageindex.html

NOTE:Hospitals may also appeal denials of MGCRB decisions to the CMS Administrator. Hospitals have 45 daysfrom the date the IPPS proposed rule is issued in the Federal Register (published in Federal Register on August 17, 2018) to decide whether to withdraw or terminate an approved geographic reclassification for the following year.

{kind=link}